Mostly Human Economic Analysis: July 2025

News & Updates

|August 8, 2025

Introduction: Strong Spending Continues Amid Gloomy Expectations and Hesitant Businesses

Since the pandemic, business leaders and analysts have been watching closely, expecting consumer behavior to eventually shift. After all, 2020 and 2021 brought an unusual mix: stimulus checks, cheap credit, and a flood of liquidity into the economy. That kind of environment isn’t sustainable so the assumption was that spending would eventually slow.

But here we are, with interest rates up, lending tighter, pandemic-era support long gone, and consumers are still spending. They haven’t really pulled back, changed what they buy, or become significantly more cautious. They’re just… keeping at it.

When we look at post-pandemic trends, we’re always asking the same question: has this behavior snapped back to its old trajectory, or are we still seeing lasting disruption? If a trend has rejoined its pre-2020 path, we can call that a return to “normal.” But if it’s still elevated, lagging, or off course that tells us the pandemic left a more permanent mark.

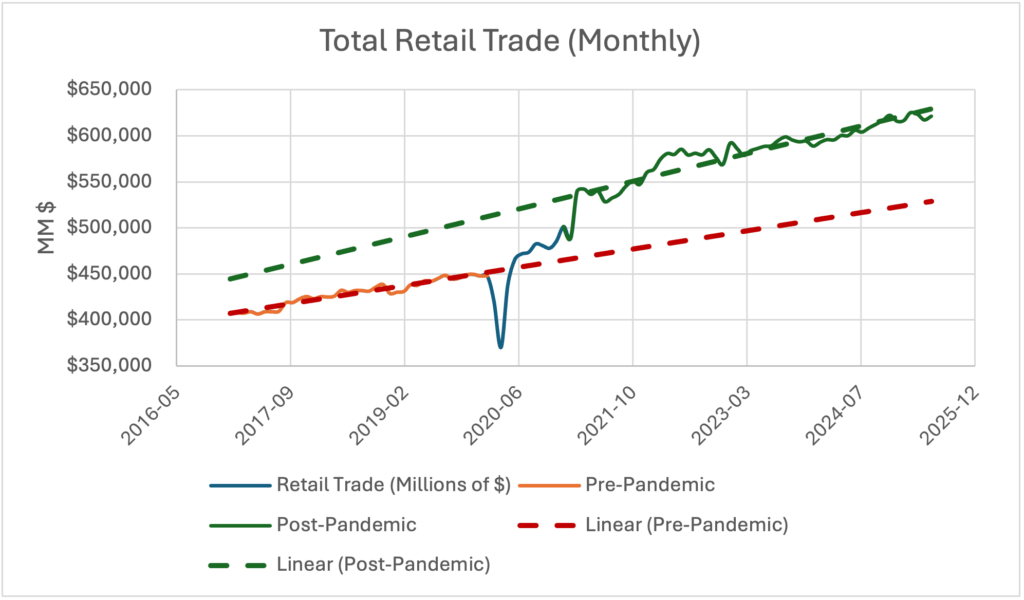

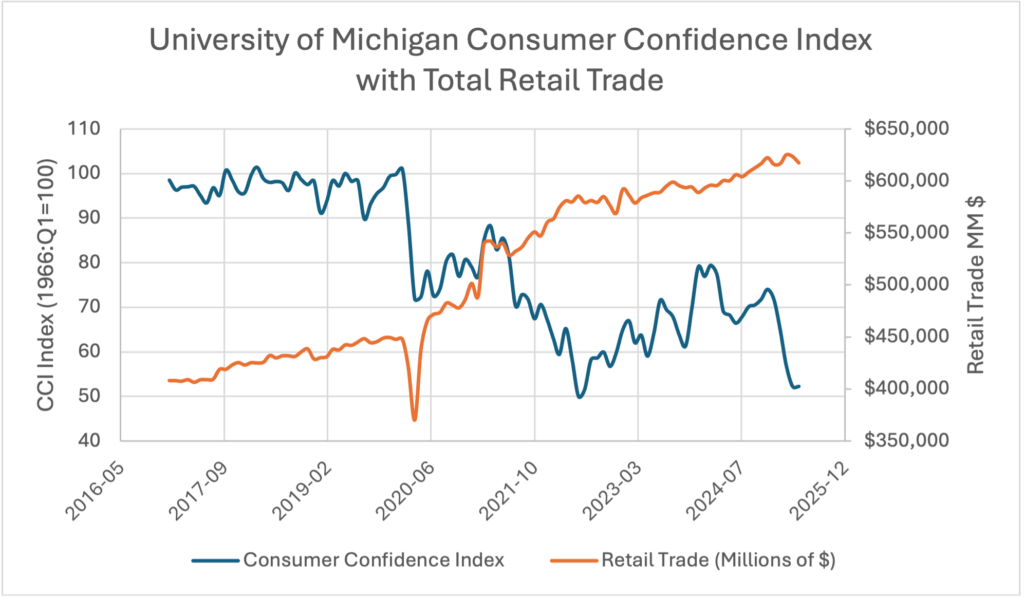

Retail trade, for example, has reset to a significantly elevated post-pandemic baseline along with an acceleration in growth rate (See above). We can confidently say that retail growth has and continues to exist in a markedly different (and positive for businesses) post-pandemic norm.

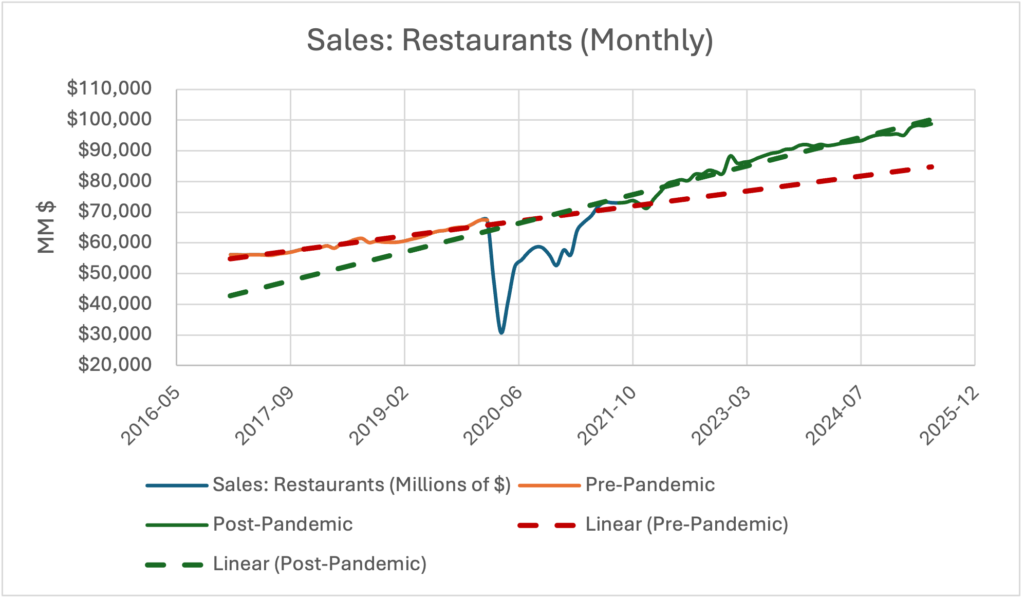

Restaurants on the other hand have more so rejoined their pre-pandemic trend. There has been an acceleration in growth, it’s been a persistent story that consumers have been more consistent and adventurous in visiting restaurants since the pandemic. Additionally, prices are up and there’s no indication they’ll drop in relative terms. However, restaurants remain constrained by population and capacity much more so than other industries.

As we’ve noted, the trendline has accelerated somewhat, but without the corresponding reset to the overall level of consumption evident in the retail example.

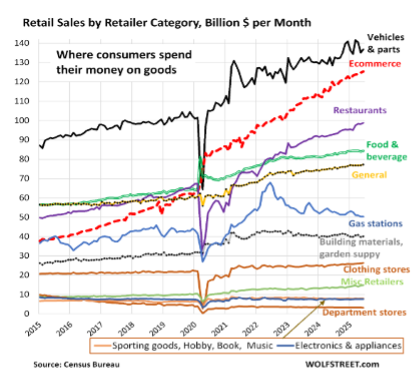

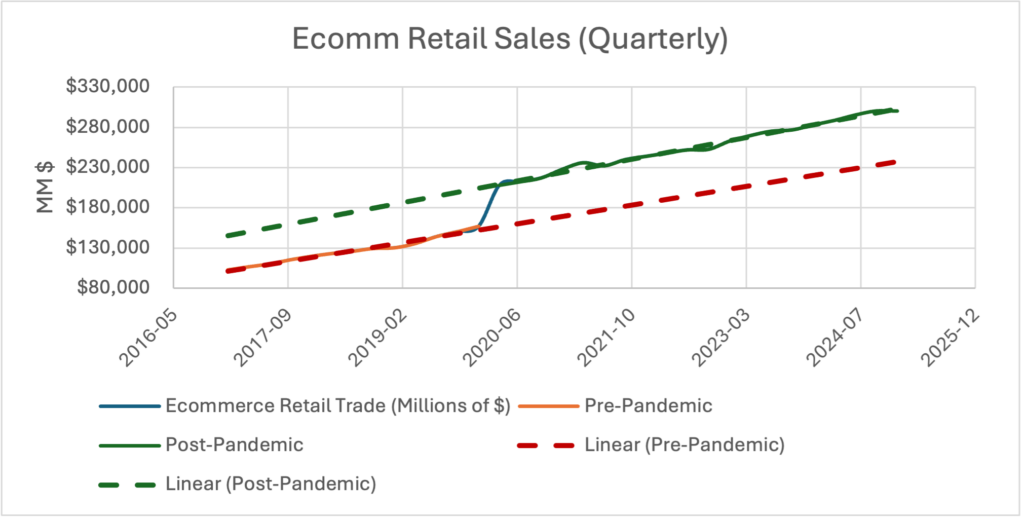

Sales Are Rising Across Industries Despite Uncertainty and Persistent, Negative Expectation

Let’s look at Ecomm alone as an example:

Ecommerce businesses have not been immune from component price hikes and other economic headwinds and yet demand has skyrocketed since the pandemic with no indication of slowing down. This accounts for a large amount of retail growth, but it has not cannibalized in-store as many would suspect.

What About Consumer Confidence?

Consumer confidence is near an all-time low in 2025. Consumers do not like the uncertainty of potential price and interest-rate fluctuations. Tariffs seem to have had a particularly large negative impact on consumer confidence in recent months although additional data is needed to fully validate that assessment.

The data shows this has little impact on behavior in the macros sense, especially in recent years. Consumers have continued to spend despite a step change (or two) in economic confidence since the pandemic.

Consumers Are Flush with Cash and Credit

Consumers keep spending despite perceived economic headwinds because, despite the noise, their finances remain in relatively good shape, at least in aggregate. Incomes have been growing for years, jobs are plentiful, and people have used pandemic cash and other programs to reduce debt and build savings.

Available credit has increased significantly in recent years. Credit card balances have increased as well but at a much slower rate.

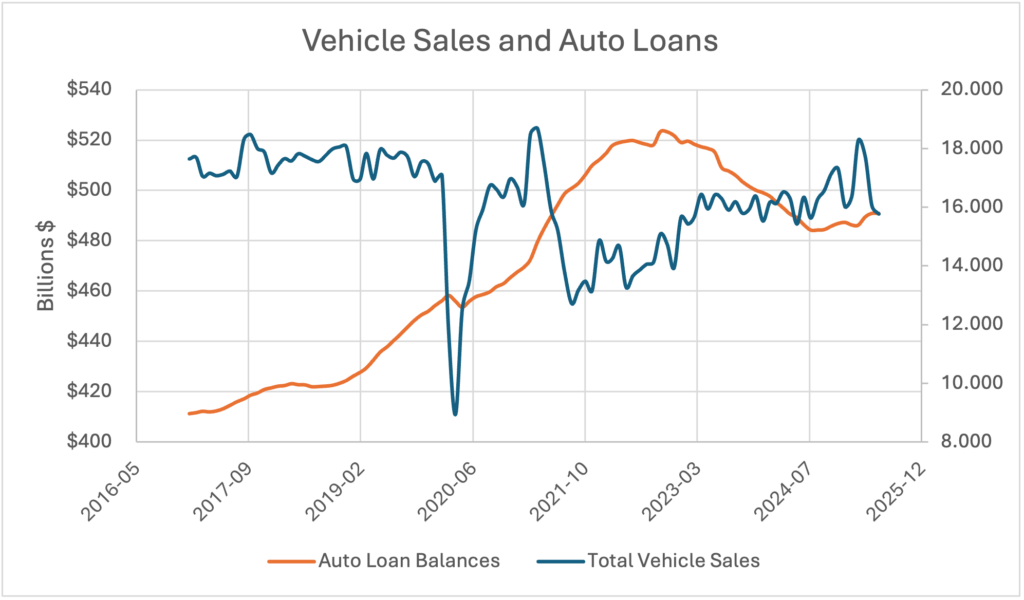

Auto loan balances have trended down as well, as consumers increasingly opt to purchase with cash.

Notably, purchase volume is trending up towards its pre-pandemic level, while loan balances are markedly down since the pandemic. People are buying cars and prices remain high, they’re just using cash and avoiding finance costs.

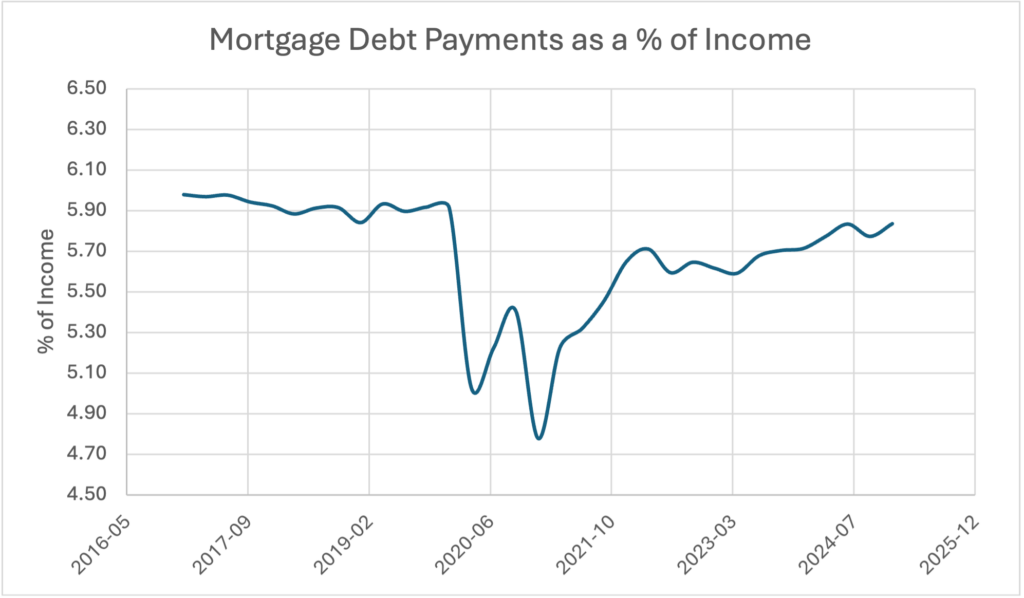

The good news doesn’t stop there… Mortgage loans have trended down as a percentage of disposable income. Home prices have increased steadily, and sales have remained strong despite returning from the post-pandemic peak, however mortgage servicing costs have not outpaced income growth.

Big-Ticket Purchases and “Selective” Spending

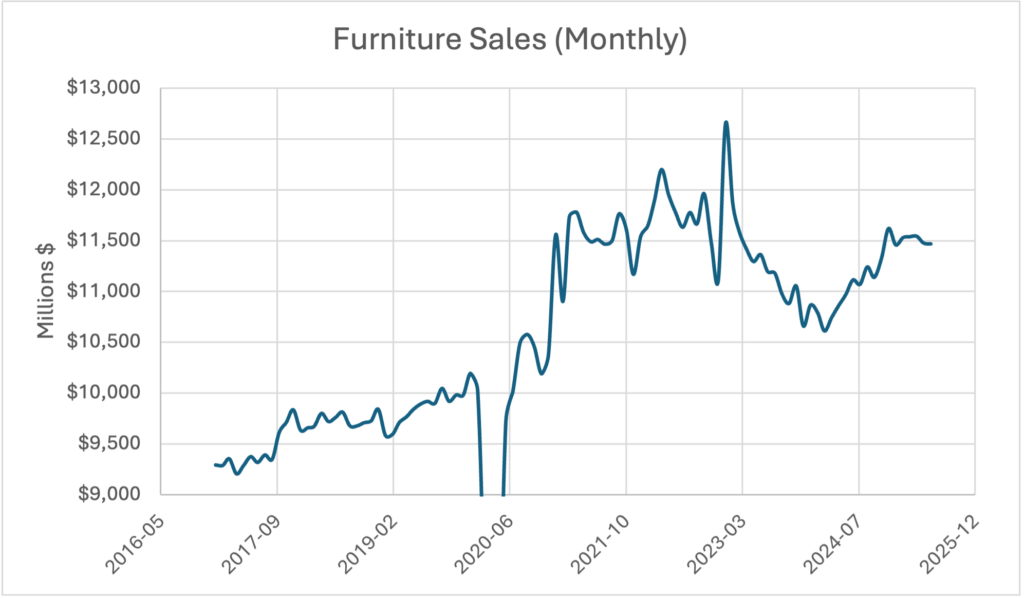

Big-ticket purchases can be difficult to track. Furniture is generally a good non-vehicle item as it is high value, can be financed, and has a longer purchase and consideration cycle.

Furniture sales have essentially returned to business as usual after a significant pandemic driven peak. They’ve seen strong sales over the past 15 months after a protracted downward trend post-pandemic. There’s no indication that people aren’t purchasing and if anything, we can attribute much of the 2023-2024 slump to pulled ahead purchases made in 2021-2023.

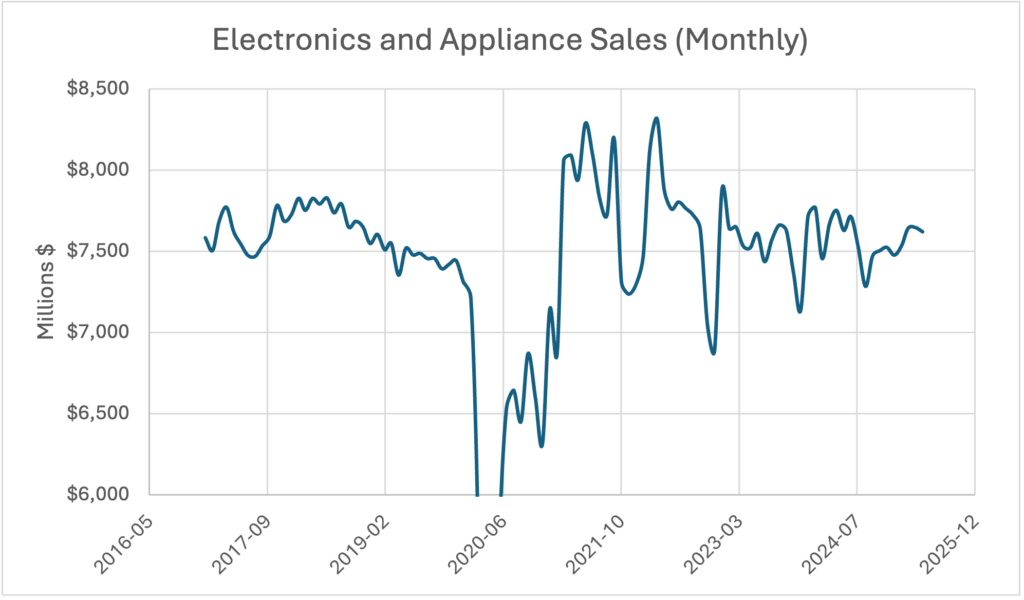

Electronics and appliances are another good example of big-ticket, discretionary items. Like furniture, there is a base level of sales with additional purchases shifting with consumer demand and disposable income.

Again, electronic sales are generally in-line with pre-pandemic levels, with a bit more variability. Therefore, there’s no indication here that consumers have stopped spending.

Based on these examples, along with vehicle sales, consumers are not notably delaying or foregoing big-ticket purchases. A full assessment is noisy and nuanced, but there is no clear indication that consumer purchasing behavior is changing in 2025. It’s certainly not clearly trending down or giving any indication of fiscal tightening.

Will Tariffs Drive Inflation? They Should, Shouldn’t They?

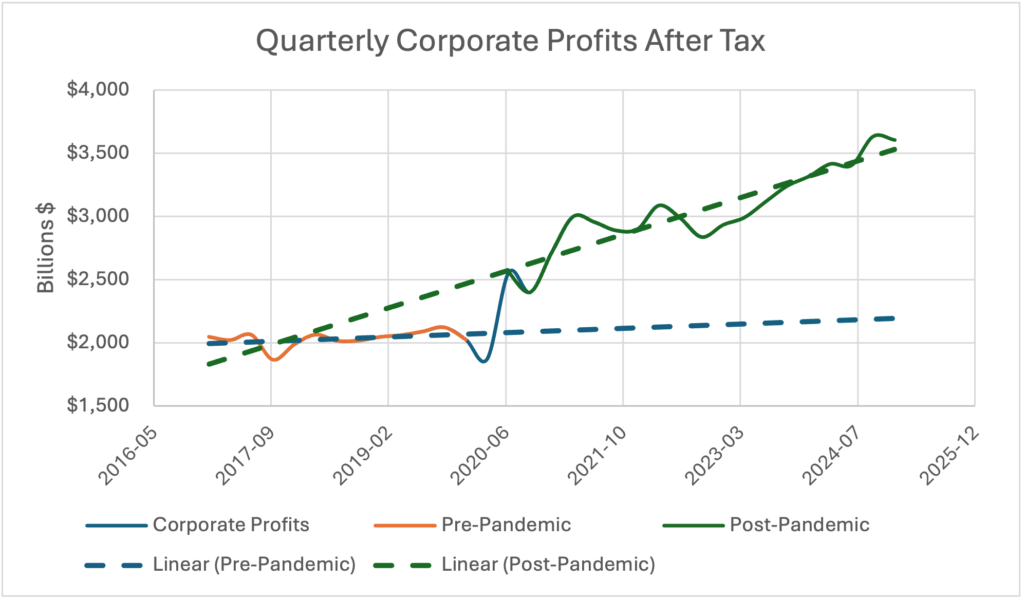

We’d argue that it’s a pretty simple question, but not in the way that you think. To illustrate our point, let’s look at corporate profits pre and post-pandemic.

Corporate profits have increased 78% from Q1 of 2020 to Q1 of 2025. Let’s say that one more time. Despite all the talk of component costs, supply chain disruptions, and shortages, corporate profits have nearly doubled in the last 5 years. Businesses have enormous fiscal space to absorb tariff driven price increases and, interestingly, they generally have to this point. The question is, will that continue and if it doesn’t, will consumers accept additional inflation or push back. Does it even make sense for businesses to absorb these costs given the ire of consumers has been directed squarely at political rather than business leaders?

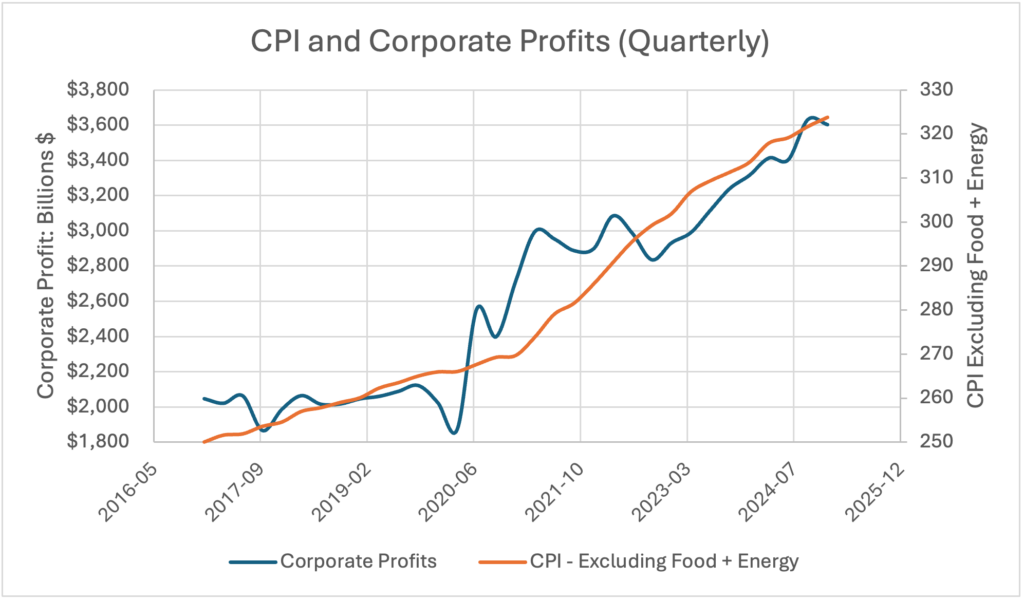

Future questions aside, how does that correlate to the inflation that we’ve seen over the past few years?

To put it simply, corporate profits drove inflation since the pandemic. So, it’s really up to business leaders to decide how tariffs impact consumers.

This is an exceptional position to be in as businesses can essentially control demand based solely on price elasticity and profitability. If businesses are flexible and reactive they can set the market with minimal risk to volume or profitability.

Clearly, significant tariff driven costs, if they come to pass, will impact prices or profitability, but it’s essentially 100% up to businesses who feels that impact and to what degree. They can maximize profit given the environment if they are diligent and reactive enough to do so.

Outlook: Q3 2025 and Beyond

All the data above paints a consistent picture: the US consumer is financially healthier and more resilient than many assume. Despite years of rising interest rates, persistent inflation, and the end of stimulus, consumer spending has continued to grow and shows no indication of slowing absent some extreme disruption.

Of course, no one is saying the consumer is invincible. High interest rates do price out some marginal buyers and student loan payments restarting could limit budgets. There’s also an upper limit to how long savings can prop up spending, but for the time being the economic outlook points to consumers largely shaking off these challenges and marching forward.

Consumers are ready to spend, and brands should not hesitate to lean-in and expect a strong return on customer-focused investments.

If anything, businesses should be careful not to underestimate consumers’ willingness to spend. The pessimistic sentiment has repeatedly been disproven by consumers’ actual behavior.

What Should Brands Do?

- Capitalize on this moment. Make investments now while profitability is high and customers are shopping.

- Know the metrics that matter. Sales, traffic, and margins matter. Maintain those metrics and…

- Ignore metrics that don’t matter or impact your business. Consumer confidence and inflation haven’t hurt consumer spending yet, so why would they going forward.

- Be flexible with your customers. For example, customers aren’t financing as much as they used to so don’t lean into financing offers in your positioning.

- Do what your competitors won’t. Don’t pass all costs on to your customers. Advertise and offer value despite perceived economic and policy headwinds. Give your customers an avenue to spend and they will.